Click here to get the 2016 Southern California Assessment Appeals Filing Deadlines

California Property Tax Overview

If you have questions or think your property is over taxed give us a call! We’d love to have the chance to represent you. Put our 25+ years of successful property tax appeals to work for you.

Please click on any link in the table below to be taken immediately to that section.

ANNUAL ASSESSMENTS

The assessor’s primary responsibility is to annually determine the proper taxable value for each property so the owner is assured of paying the correct amount of property tax for the support of local government.

The county assessor must annually assess all taxable property in the county, except for state-assessed property, to the person, business, or legal entity owning, claiming, possessing, or controlling the property on January 1. The duties of the county assessor are to discover all assessable property, to inventory and list all taxable property, to value the property, and to enroll the property on the local assessment roll.

The assessor must reassess real property to current market value whenever there is a change in ownership or completed new construction. In addition, the assessor may change the assessed value of a property to recognize a decrease in value, to correct an error, or to enroll an escaped assessment (one overlooked previously). Except for changes in assessment due to annual adjustments for inflation, assessors must notify property owners whenever their assessments of real property are increased. The notifications are sent on or before the date the assessment roll is completed, generally July 1. Valuation notices contain important information about your property, including the value as of January 1, referred to as the “lien date”. Separate notices are mailed for special assessments, referred to as “supplemental”, “revised”, “calamity” or “escape” assessments.

Personal property is reassessed annually. Notification of personal property assessments is not required.

In preparing the assessment roll, the Assessor Department estimates a property’s full cash value. Appraising is not an exact science, but is an opinion based on consideration of relevant facts.

The Assessor will lower the assessed value of any real property if it is higher than the current market value as of lien date. Each case is reviewed individually upon the filing of a Decline-in-Value Reassessment Application.

ASSESSMENT APPEALS

Any property owner who disagrees with the assessed value of his/her property may file an appeal.

Ifthe assessed valueof your property is higher than market value, you are over-assessed andentitled to an assessment reduction. Additionally, exclusions or exemptions from reassessment may have been warranted butnot applied.

The assessed value of your property multiplied bythetax rate equalsyourpropertytax liability. Therefore, a reduction in your assessed valuelowers your property taxes.The Assessment Appeals process concerns only the assessed value of your property. Tax rates are not subject to dispute and are determined each year by the Auditor/Controller.

Any property owner who disagrees with the assessed value of his/her property may file an appeal. Although not required, a property owner may have an attorney, family member or professional tax agentfile on his/her behalf. In fact, in California, anyone properly authorized can represent any owner on an assessment appeal of a property.

Differences of opinion can and do arise. Property owners have the right to challenge their property assessments by filing an Application for Changed Assessment with the Assessment Appeals Board.

An Application for Changed Assessment (formal assessment appeal) is your opportunity to challenge the assessed value placed upon your property by the Assessor.

Most California counties do not charge a fee for filing and processing assessment appeal applications. However, this trend is quickly changing. In Southern California, both Riverside and San Bernardino Counties currently charge small filing fees ($30 & $45 respectively per parcel). Please contact individual counties for their filing fees.

Assessment appeals filing periods are very short. If youmiss thefiling deadline, you will miss out on potential tax savings or refunds!

Applications for “APPEALS OF REGULAR ASSESSMENTS” (value as of January 1 of the current year) must be filed with the Clerk of the Assessment Appeals Board between July 2 and no later than September 15 or November 30 each year (depending on county). If the date for the end of the filing period falls on a Saturday or Sunday, then the last date to file will default to the date of the following business working day.

Applications for “SUPPLEMENTAL”, “ROLL CHANGE”,or “ESCAPE”assessments must be filed no later than sixty (60) days from the Assessor’s Notices, or mailing date of supplemental tax bill. Filing deadlines vary by county, so check with your local assessor’s office to see which deadline applies.

Applications for “CALAMITY” assessments must be filed no later than six (6) months from the Assessor’s Notice of Reassessment Due to Calamity or Misfortune.

Determinations of value are made by either a three member Assessment Appeals Board(AAB) or a Hearing Officer. These individuals are appointed by the Board of Supervisors to serve as the local board of equalization. They must have experience as an appraiser, real estate broker, CPA or attorney. Their role is to determine the value of your property based upon evidence presented by you and the Assessor.

Having your case heard before a hearing officer is considered an expedient and convenient alternative to the formal Board quasi-judicial proceedings. However, if you wish to have Findings of Factprepared, you must have your case heard before a full AAB Board and the appropriate fee.

Most appeals heard by an Assessment Appeals Board are scheduled within twelve to eighteen months; Residential appeals heard by a Hearing Officer are often scheduled sooner, within six-nine months. Revenue and Taxation Code § 1604 allows up to two years for an assessment appeal to be decided.

At the hearing, you and the Assessor are given the opportunity to present factual evidence to substantiate your opinions of value. All testimony is presented under oath. You and the Assessor may question each other regarding the evidence presented.

The Board will either advise you of their decision at the conclusion of the hearing or you will be notified of their decision by mail at a later date. This decision is final and may only be appealed to Superior Court.

PROPOSITION 13 – REAL PROPERTY

Proposition 13, passed in 1978, established the base-year value concept for property tax assessments. Under Proposition 13, assessments for the year 1975-76 serve as the original base year values. The maximum levy cannot exceed 1% of a property’s assessed value (plus bonded indebtedness and direct assessment taxes) and base-year valueincreases, adjusted for inflation, are limited toa maximum of 2 percent per year. Only four events can cause a reappraisal:

1. A change in ownership;

2. Completed new construction;

3. New construction partially completed on the lien date (January 1); or

4. A decline-in-value (see Decline-in-Value Review).

The taxable value for any tax year is the Prop. 13 taxable value or the market value on January 1 (lien date), whichever is lower.

Unsecured property assessments, including business personal property, boats and aircraft are not subject to Proposition 13.

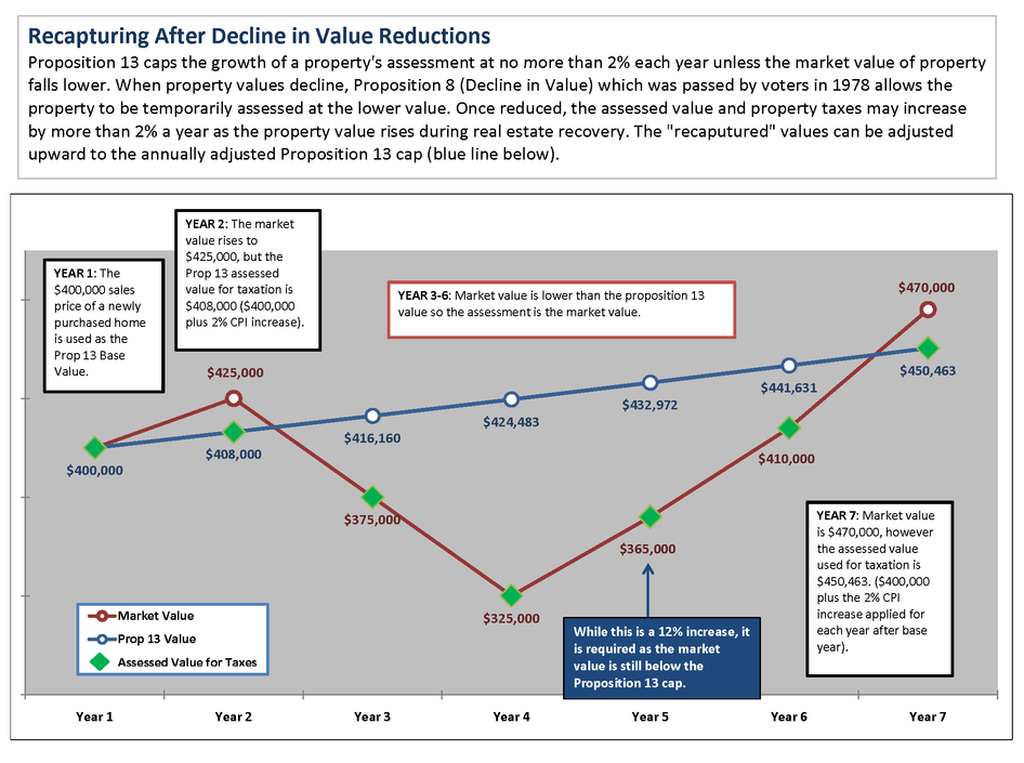

PROPOSITION 8 – Decline in Value

In 1978, California voters passed Proposition 8, a constitutional amendment that allows a temporary reduction in assessed value when a property suffers a “decline-in-value.” A decline-in-value occurs when the current market value of your property is less than the current assessed value as of January 1.

The law requires the assessor to annually enroll the lower value of either the current market value, as of January 1, or the Prop 13 base year value (factored for inflation no more than 2% annually). As the market value of the property rises, the assessed value may increase more than 2 percent a year up to the annually adjusted Prop 13 factored base year value. The assessed base year value is the full cash market value at the time of transfer of ownership, plus the incremental value ofnew construction.

Prop 8 – Decline in Value, and Prop 13 – Property Tax Limits

CHANGE IN OWNERSHIP

When a transfer occurs, the Assessor receives a copy of the deed and determines if a reappraisal is required under State law. If it is required, an appraisal is made to determine the new market value of the property.

The transfer of property between husband and wife usually does not require a reappraisal for property tax purposes. This includes transfers resulting from divorce or death. Similar to the inter-spousal exclusion, transfers between Registered Domestic Partners that occur on or after January 1, 2006, may also be excluded from reappraisal. In addition the transfer of the principal place of residence between parents and children (and the transfer of up to $1 million of any other real property between parents and children) is also excluded from reappraisal if an application is timely filed.

Transfers between grandparents and grandchildren may also be excluded from reappraisal when both parents of the grandchild are deceased. However, a son-in-law or daughter-in-law of the grandparent that is a stepparent to the grandchild need not be deceased. Some restrictions apply.

REPORTING A CHANGE IN OWNERSHIP

State law requires that a Preliminary Change of Ownership Report (PCOR) be filed when a deed is recorded. If a deed is recorded without a PCOR, the Clerk-Recorder will collect a fee and the Assessor will send a Change of Ownership Statement (COS) to the new owner.Failure tocomplete and return the COS will resulta large penalty.

NEW CONSTRUCTION

Copies of all building permits are sent to the Assessor by the city/county building departments. In appraising new construction, the market value of the addition is determined and added to the existing value of property. The value of the existing property increases only by the amount of the addition/new construction. The value of partially completed new construction is added on January 1 (lien date). Examples of new construction include room additions, patio covers, pools, spas, decks and flatwork.

The new assessed value will not change except for the annual inflation adjustment of up to 2%. As with all newly assessed values, the property owner has the right to appeal the value.

Normal maintenance, repairs or replacements of existing items is not reassessable. Replacing a roof, repairing a garage door, remodeling a kitchen will typically not increase the taxable value.

SUPPLEMENTAL ASSESSMENTS

State law requires the Assessor to reappraise property as of the date of change-in-ownership or completion of new construction. The Assessor makes a supplemental assessment which reflects the difference between the prior assessed value and the new assessment. This value is prorated based on the number of months remaining in the fiscal year, July 1 through June 30. This assessment is in addition to the regular tax bill.

The Assessor mails a Notice of Supplemental Assessment directly to property owners. Thereafter, the Tax collector mails a Supplemental Tax Bill. Supplemental taxes are not paid in escrow.The Supplemental Tax Billdoes not replace or cancel the annual tax bill.

More on Supplemental Assessments

MANUFACTURED HOMES

All manufactured homes purchased new after June 30, 1980, and those on permanent foundations, are subject to property taxes. As with real property, the assessed value of manufactured homes cannot be increased by more than 2% annually, unless there is a change-in-ownership or new construction.

Many manufactured homes, originally built and sold before June 30, 1980, are on the in-lieu tax system administered by the State Department of Housing and Community Development (HCD).

BUSINESS AND PERSONAL PROPERTY ASSESSMENTS

In California, business and personal property, including boats, airplanes, and certain restricted properties are appraised annually andsubject to property taxes. Business personal property includes, but is not limited to: machinery, equipment, furniture, computers, printers, copiers, telephones, fax machines, supplies and leased equipment.

Businesses are required by law to report the cost and year of acquisitions of all business personal property (owned or leased), trade fixtures and supplies for each business location on an annualBusinessProperty Statement (BPS). Each year Business Property Statements, which provide a basis for determining property assessments for fixtures and equipment, are mailed by the Assessor to most commercial, industrial, and professional firms. Businesses with personal property and fixtures that cost $100,000 or more in any assessment yearmust file a BPS each year by April 1. The last day to file a BPS without incurring a 10% penalty is May 7.

Generally, businesses with personal property and fixtures that cost less than $100,000 are not required to file a Business Property Statement annually. Instead, a value is established based on an initial Business Property Statement filing or by an on-site appraisal. That value may be adjusted by subsequent annual on-site appraisals.

Business inventory is exempt from taxation.

More on Business Personal Property Assessments

MARINE AND AIRCRAFT

Boats and airplanes are taxable and appraised annually. Their value is determined by reviewing the purchase price and the sales of comparable boats and airplanes. Information of their location and ownership is obtained from the Department of Motor Vehicles, the Federal Aviation Administration, Fixed Based Operator (FBO) Reports and on-site inspections. State law requires that boats and airplanes will be assessed on January 1, starting 1997 and for each year thereafter, at the site where they are regularly or routinely located. All boats and airplanes are assessed in the county where they are regularly located, regardless of where they are registered.

More on Boats & Aircrafts Property Tax

Exemptions, Exclusions and Tax Relief

Exemptions, Exclusions and Tax Relief

HOMEOWNERS’ EXEMPTION

If you own a home and occupy it as your principal place of residence on January 1, you may apply foraHomeowners’Exemption of $7,000 of your assessed value. This will reduceyour taxablevalue by $7,000 and will save you at least $70 per year on property taxes.New property owners should automatically receive an exemption application in the mail. Homeowners’ Exemptions may also apply to a supplemental assessment if the property was not receiving a Homeowners’ Exemption previously on the regular Assessment Roll.

BUILDERS’ EXCLUSION

New construction built specifically for sale may be excluded from supplemental assessment. If the property is held for resale, has five or more lots and is zoned or permitted for single family residential development, no claim form is necessary. However, for properties of less than five lots or those zoned or permitted for non-single family residences, the property must be held for sale and the builder must file the necessary claim form with the Assessor prior to or within 30 days from the start of construction. If the form is not filed, a supplemental assessment is made to the builder upon completion of the construction. If the form is filed, a supplemental assessment is not made until the property is sold to the new owner. This exclusion does not affect assessment of new construction on the regular assessment roll.

VETERANS’ EXEMPTIONS

- A $4,000 exemption for any property that is owned by an eligible veteran and is subject to property taxes. This exemption can be applied to real estate, a boat, or plane, or property used in a trade, profession or business.

- This exemption is also available to a surviving spouse and/or the parents of a deceased veteran.

- Because the Homeowners’ Exemption of $7,000 provides greater savings than this one, most California veteran homeowners choose the Homeowners’ Exemption.

DISABLED VETERANS’ EXEMPTION

- This exemption applies to the home of a person (or a person’s spouse) who is, or has been, injured in military service.

- In general, injuries that qualify a veteran for the exemption include: (1) total disability, (2) blindness, or (3)has lost the use of two or more limbs.

- The amount(s) of the exemption depend upon: (1) the type of injury, and (2) the household income.

- A 100% disabled veteran is allowed a Basic Exemption of $126,380 with no income limitation for the 2015 lien date.

- A 100% disabled veteranis allowed a Low-Income Exemption of$189,571, with a household income limit of $56,751 for the 2015 lien date.

More on Disabled Veteran’s Exemption

INSTITUTIONAL EXEMPTIONS

Property used exclusively for a church, college, cemetery, museum, school or library may qualify for an exemption. Properties owned and used exclusively by a non-profit religious, charitable, scientific or hospital corporation are also eligible. A claim must be filed.

The Legislature has the authority to exempt property (1) used exclusively for religious, hospital, scientific, or charitable purposes, and (2) owned or held in trust by nonprofit organizations operating for those purposes. Whether the organization’s operations are for one of the above purposes is determined by its activities and subject to other requirements. A qualifying organization’s property may be exempted fully or partially from property taxes, depending on how much of the property is used for qualifying purposes and activities.

More on Institutional Exemptions

EMINENT DOMAIN

This provides that if a government agency acquires property through condemnation, owners have the right to retain their existing value and transfer it to a replacement property. The replacement property must be comparable to the property acquired, and an application form must be filed with the Assessor within four (4) years from the date of acquisition. See Prop. 103.

More on Eminent Domain

REAPPRAISAL EXCLUSION FOR SENIORS AND DISABLED

In many California counties, disabled property owners orsenior citizens over 55 years of age can buy a residence of equal or lesser value than their existing home and transfer their current assessed value to the new home. See Prop 60, 90, & 110.

More on exclusions for Seniors & Disabled

PARENT/CHILD, GRANDPARENT/GRANDCHILD EXCLUSION

The transfer of real property between parentsand children or from grandparents to grandchildrenmay be excluded from reappraisal. See Prop58 & 193.

-

- No limit is placed on the assessed value of a principal residence that may be excluded from reassessment.

- In addition to tax relief on the principal residence, you may claim an exclusion on transfers of other real property with anassessed value of up to $1,000,000.

- A claim mustbe filed within3 years of the date of transfer to receive the full benefit of the exclusion.

More on Prop 58 & 193

DISASTER RELIEF

If a major calamity, such as fire or flooding, damages or destroys your property, you may be eligible for property tax relief. In such cases, the Assessor’s office will reappraise the property to reflect its damaged condition. In addition when you rebuild it in a like or similar manner, the property will retain its previous value for tax purposes.

To qualify for property tax relief, you must file a calamity claim with the Assessor’s office within 12 months from the date the property was damaged or destroyed. In addition, the loss must exceed $10,000.

LAND CONSERVATION- WILLIAMSON ACT

The California Legislature passed the Williamson Act in 1965 to preserve agricultural and open space lands by discouraging premature and unnecessary conversion to urban uses. The Act creates an arrangement whereby private landowners contract with counties and cities to voluntarily restrict land to agricultural and open-space uses.In return, restricted parcels are assessed for property tax purposes at a rate consistent with their actual use, rather than potential market value.

HISTORIC PROPERTIES- MILLS ACT

Adopted by the California Legislature in 1976, the Mills Act gives local governments the authority to grant property tax relief to owners of qualified historic properties, including owner-occupied and income producing properties. In exchange for this relief, the property owners must agree by contract to maintain the properties in accordance with specific historic preservation standards and conditions.

SOLAR NEW CONSTRUCTION

Under certain circumstances the initial purchaser of a building with an active solar energy system may qualify for a reduction in the assessed value of their property.

More on Solar New Construction

COUNTY ASSESSOR’S PARCELMAPS

CountyAssessor’s offices establish and maintain sets of maps for assessment purposes, delineatingall parcels of land in the county. These maps serve as the basis for the assessment of all real property. The maps are continuously updated to reflect new subdivisions and parcels.

IMPORTANT PROPERTY TAX DATES

January 1: Lien date – the time when taxes for the following fiscal year (July 1 – June 30) become a lien on property.

February 15*: Deadline for filing Veterans’, Homeowners’, Church, Religious, Welfare Exemptions, Historical Aircraft and other institutional exemptions.

April 1: Deadline for filing Business Personal Property, Boat, and AircraftStatements.

April 10*: Deadline for payment of second installment of secured property taxes.

May 7*: Last day to timely file aBusiness Personal Property Statement without penalty.

July 1: Assessment Roll delivered by the Assessor to the Auditor-Controller.

July 2 – September 15 or November 30*: Period during which the Clerk of the Board accepts petitions for Assessment Appeals Board hearings on the regular roll. (Other filing periods may apply for supplemental assessments and escape assessments.)

August 31*: Deadline for payments of unsecured property taxes.

December 10: Deadline for late filing of Homeowners’, Veterans’ and Disabled Veterans’ Exemptions. Deadline for payment of first installment of secured property taxes.

*If the date falls on a weekend or holiday, the deadline is extended to the next business day.